Dispelling Market Myths

Down markets and the tangents they bring us on

Welcome to the 5 new Thinkers who joined ThinkingCap, thanks for continuing to share this with friends, we’re now 94 strong 💪

Greetings from Italy,

There’s no better time to deal with a down market than while on vacation. Any excuse to go back to enjoying what’s within my field of vision is a valid one.

So I closed my browser, enabled Airplane mode, and opened a fresh note. Alas, what better time to talk about how investing greats like Bogle, Malkiel, and Buffet would approach a down market?

As I started typing, I couldn’t help but cross-referencing some of my notes and ensuring the axioms passed onto me were still relevant. It’s human-nature to think “this time is different,” and I was chock full of those feels. So I dug in and what started as a well-intentioned “hang in there” morphed into 🧐

Your mission, should you choose to accept it is to reconsider and challenge investing axioms embedded within you.

Here are three from my side:

Market timing

Compounding returns

Professional help

Time in market versus market timing

Let’s start with market timing. We’ve heard the quote before, “it’s time in market not timing the market” that determines success. While there’s empirical data to support this, it’s leveraged as a de facto response to all market timing objections. I’m not here to encourage market timing, nor am I a financial advisor, but equipped with the resources of an ever growing internet, I was able to find some data supporting market timing. Bank of America calculated S&P500 returns in three theoretical scenarios:

Excluding the 10 worst days of each decade

Excluding the 10 best days of each decade

Excluding both the 10 best and the 10 worst days of each decade

While I expected Scenario 1 to exceed baseline, and Scenario 2 to fall short of baseline, I didn’t know what to expect or scenario 3. Turns out, Scenario 3 outperforms baseline returns, and it’s fairly significant: 17,715% baseline vs 27,213% when excluding both the 10 best and the 10 worst days of each decade.

Again, not encouraging you to time the market, but it does serve as interesting psychological fodder — seemingly suggesting that the lows are more extreme than the highs, at least when looking at a full S&P500 index. While individual companies may have breakout days, it’s believable that macro conditions combined with mimetic capitulation are the most aggressive market movers.

Don’t let that scare you, ultimately our baseline investor still walks away with a 17,715% return showing that the true magic here is the compounding happening during these decades. A perfect segue into our next myth:

The fickle magic of compounding

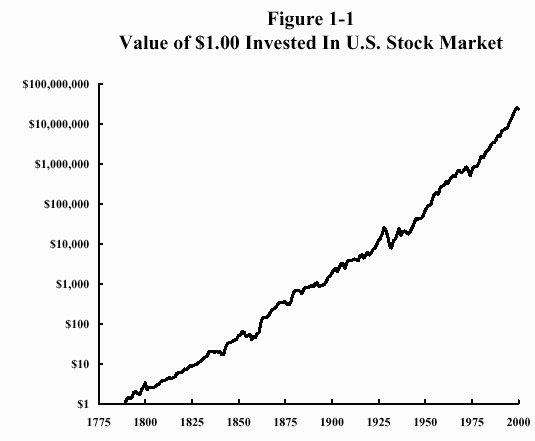

Conventional investing wisdom is quick to reference the magic of compounding. Charts like the one below make you wish that your grandparents were spending their disposable income on stocks and bonds versus doilies and cookie jars. The problem with these delusions of compounding is that they don’t take into account two key aspects of investing:

We invest money now in hopes of having more money later. Therefore you or your heirs will likely withdraw funds at some point.

Even the slightest of fees can greatly impact our compounded returns.

Point one is self-explainable so let’s jump into point two. The chart below shows the value of a single dollar invested into the US Stock Market from 1790 to 2000.

$1 grows to an astonishing $23M+, this is the “fairy tale” promise of compounding.

I hate the FOMO created by these charts. As easy as it is to say today that you should invest in the US Stock Market, this chart starts pre-Civil War. The US economy was a far cry from what it is today and most investors at the time may have considered a 100% allocation into the US Market irresponsible.

Even if you managed to make the investment it still ignores brokerage fees, taxes, and commissions from a financial advisor. In Efficient Frontier, William Bernstein writes:

Because of the mathematics of return compounding, spending even a tiny fraction on a regular basis devastates final wealth during very long periods: over two centuries, each one percent spent each year reduces the final amount by a factor of eight. For example, a 1% reduction in return would have reduced the final amount to about $3 million, a 2% reduction to about $400,000.

That’s right, $23M+ reduced to ~$3M from a measly 1% annual fee. Compounding is one hell of a drug.

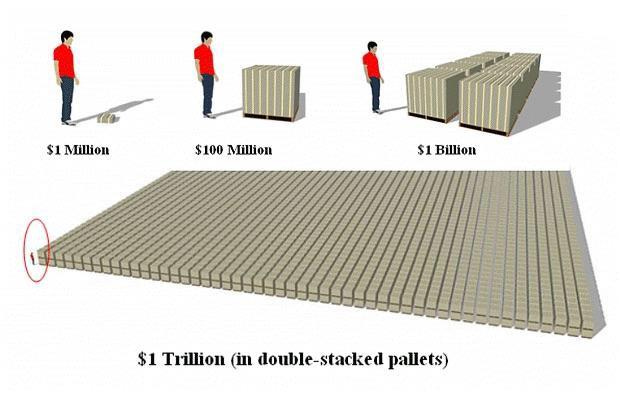

Exponentials are difficult for our brains to comprehend, hence despite seeing this diagram many times before, it’s still visually shocking to see how small $1M is compared to $1T.

Given the complexity and confusion, we must enlist professional help right?

Maybe not. In my last issue (here) I detailed Warren Buffet’s wager with Hedge Funds that over 10 years the S&P500 will outperform them. Buffet won that bet and continues to recommend low-cost S&P500 Index Funds (Vanguard is a great place to start your research). Even if he didn’t, we now see how costly even a 1% fee can be over the long term when we factor in compounding.

While I haven’t personally worked with a professional financial advisor, I know that there’s a wealth of information out there to help us help ourselves. That said, I have seen firsthand the merits of working with an accountant, various real estate brokers, and other professionals. Just keep in mind the opportunity cost of the fees you’re paying for these services and how that will impact your returns over the long run.

Sources and additional reading

Bank of America chart via CNBC (link)

Figure 1-1 via Efficient Frontier (link)

Visual dollar amounts comparison (link)

A slight diversion…

Back in the days of StumbleUpon — a browser extension that would suggest webpages personalized for you based on prior up/down votes — there were a few consistent up-vote silver bullets for me. One of which, were lists of words that cannot directly translate from one language to another. Words that really spoke to the culture of people in a way that was so unique to them.

A few Italian words give me that same sense, but none are as fun to say as “boh!” “Boh”, is a one-stop-shop response to express that they don’t understand something. The same way you might use “idk” on a text message, or say “dunno” IRL, yet “boh” is used by people of all ages, and combined with the expressive gesturing that typically accommodates it, it’s such a easy phrase to comprehend regardless of your Italian language proficiency.

What’s your favorite word that cannot be translated?

Until next Thursday!

<$ Armand